Cover

Growth stack for Telegram builders.

B2B SaaS for the supply side. Consumer marketplace for the demand side. AI-native, on the same surface.

Telegram is the focus. Deepest distribution, native economy (Stars · TON · Gifts · partner programs), and the wave is right now — Durov back to TON, Functions / agentic-dev launch, AI-coding tools delivering builders.

The framing «messenger / superapp ecosystem with native mini-apps» is structural — same builder problems exist anywhere this category exists. We expand through the creators we already onboard, not by re-pitching new platforms (slide 09).

Audience

Hundreds of thousands of creators × their like-minded communities = tens of millions of users.

Each creator ships an app for the few hundred who think like them. Multiplied — bottom-up scale that no top-down platform can reach.

The instinct is to imagine a Telegram-app builder as a vibe-coder or a crypto founder. That's outdated. The wave underneath is any expert who serves a niche community — small-business operator, teacher, vet, fitness coach, hobbyist, niche professional. Each of them carries authority and pull within their circle.

The math is bottom-up: 1 creator × 100-1K followers × 100K-1M creators ≈ tens of millions of end-users. Top-down platforms can't reach these niches — by definition, the niches are too small individually. We don't try to reach them; we equip the creators who already serve them.

«We don't go find the housewives. We give the one housewife who already runs that community the tools to ship her app — and her community follows.»

Status quo

The launch cycle today — even early-adopters who ship are too weak to continue.

Tools eat the budget. Marketing has nothing left. Without traction, no resources to iterate. Without iteration, no traction. The cycle starves itself.

Six stages, six chances to fail. The drop-off isn't only about technical skill — most happens at marketing (50 → 15 — services consumed the budget) and at iteration to PMF (15 → 3 — exhaustion + zero feedback signal kills the loop).

Hidden cost: TIME. Most builders are part-time. Weeks of stitching → can't afford another quarter to iterate. The system rewards capital + technical skill + idle time, not insight.

«The 100K-1M niche creators from slide 02 don't fail because their ideas are wrong. They never reach the cycle.»

Insight

Replace ~10 services with one perimeter.

The remainder lands as marketing through @appss.

The deeper play isn't $200 → $30 savings — it's where the saved $170 lands. Builders who consolidate onto Apps Pro keep an active marketing budget. We make that budget land on @appss-native channels: our influencer marketplace, App Store featured slots, partner programs, bounty pools.

This is why slide 05 has 5 revenue streams instead of 1. The SaaS subscription is the floor; the redirected marketing spend is what compounds. And the more apps shipped through us (slide 04 flywheel), the more marketing-budget volume runs through these channels.

«You're not paying for tools. You're paying for the app you create — and growing it through us.»

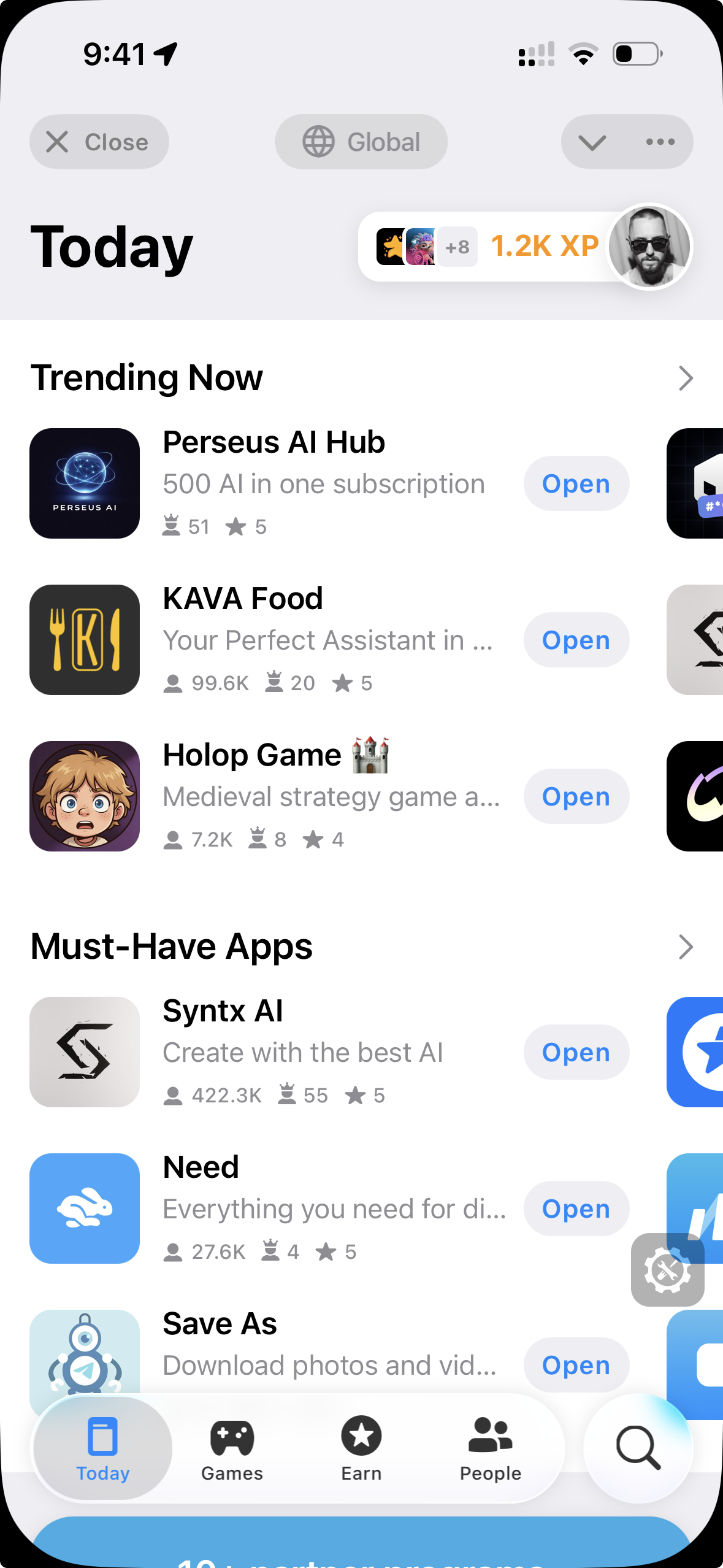

Product

Two products. App Store for users. Apps Pro for builders.

save the appss.pro screenshot here ]

$19-34/mo

App Store — Mini App in Telegram. ~5K apps in catalog, 6 languages, 5 regions. Native earn loop (Stars staking, partner programs, bounty pools) keeps users coming back daily.

Apps Pro — credit-based SaaS. Each block replaces a Western-stack equivalent (Mixpanel, Figma, Customer.io, Intercom, etc.). Market Research AI is the hero entry use-case driving current revenue.

The two share one backbone (platform-service · SDK · builder-api · TON · Stars) — which is why the next slide is the flywheel, not just «two products».

Compounding

The flywheel — every component feeds the loop.

Three loops compose: (1) Supply / Demand — more builders → more apps → more users → more demand. (2) Distribution exchange — founders amplify via our referral / vote tools and trade a share of their existing audience for new traffic. (3) Data network effect — more apps → richer market data → Market Research becomes the obvious entry tool → more builders.

Why founders accept the trade. Net-positive: more new users than they give up, plus they get $200-400/mo of tools bundled at ~$30/mo. Asymmetric in their favour.

«A pure SaaS doesn't have the App Store. A pure marketplace doesn't have Apps Pro. We have both — and they feed each other.»

Comparable

Lovable closed «build» for the web. We close the whole launch cycle for Telegram.

If one slice (vibe-code web apps) became a generational success, the whole cycle in a 1B-user ecosystem is structurally bigger.

- Chat-based web app generator

- Stops at «you have a built site»

- Founder owns: brand, host, analyse, market, monetise, support, iterate — separately

- ✓ Vibe-code (Builder + AI-tool connectors)

- ✓ Brand & list (Designer + App Store listing)

- ✓ Analyse (Pro Dashboard, native to Telegram primitives)

- ✓ Monetise (Stars · TON · partner programs · bounty pools)

- ✓ Market (Push · Referral · Tracker · Influencer marketplace)

- ✓ Support (Sentry-style, in-house)

- ✓ Iterate (data feedback loop · Market Research)

Why Lovable matters as a yardstick: they hit massive ARR by automating one step (vibe-code → working web app). They didn't help with hosting, branding, marketing, support, iteration. The market still rewarded them generously — that's what one slice is worth.

Apps Pro covers all those slices — for Telegram, where the stack is more isolated AND has native monetisation primitives (Stars, TON, partner programs) that web doesn't. Lovable saved founders weeks of build-time. We save them months of build + the whole post-launch cycle.

«Lovable closed one slice. We close the cycle. Same wave, larger surface, native monetisation.»

Expansion

The same playbook ports — through the creators we already onboard.

Influencers don't live on one platform. As messenger / superapp ecosystems mature mini-apps, we follow the creators we've already attracted. Not a re-launch — an extension.

- Cross-posting on IG / TikTok / YouTube / TG already

- 30 / 20 / 50 commission, productising into in-Apps-Pro marketplace

- Reels-driven inbound proven (slide 12)

- WeChat — closest analog (mini-program ecosystem at scale)

- LinkedIn / Roblox / Line / Kakao — mini-apps maturing

- World — verified-human ecosystem in growth

Two structural reasons this expansion mechanism works without a big-bang launch:

- Creator-led, not platform-led. We're not re-pitching every ecosystem from zero. Our ~50 influencers (and growing) already have audiences spread across platforms. As mini-apps mature on those platforms, we extend with what we already have.

- The perimeter is platform-agnostic at its core. Auth · build · brand · analyse · monetise · market · support · iterate — these blocks don't need Telegram-specific primitives. Only the monetisation rail (Stars / TON in TG) needs ecosystem-specific adapters; everything else ports.

The cost of expansion is roughly «add a monetisation adapter + onboard creators already in our pipeline», not «build a new growth stack from scratch».

«Lovable is web-only and that's their TAM. Apps Pro starts in Telegram, and the same creators take us elsewhere when those ecosystems are ready.»

Money

Five revenue streams.

Two live. Two ready, awaiting volume. One structurally uncapped.

| # | Stream | State | Mechanic |

|---|---|---|---|

| 1 | Pro subscriptions | Live | Apps Pro credit-based SaaS, $19-34/mo |

| 2 | Partner-program commission | Live | Cut on CPA payouts in catalog apps |

| 3 | App Store traffic sales | Ready | Featured / promoted slots; awaits DAU |

| 4 | Influencer marketplace fee | In-flight | Productising ~50 onboarded influencers |

| 5 | Portfolio apps | ∞ Uncapped | Notspy / Cover Food / VPN — owned directly |

Streams 1-2 underwrite the floor. Streams 3-4 unlock as App Store DAU and the in-Apps-Pro influencer marketplace ship. Stream 5 (portfolio) is what makes the upside uncapped — see slide 06.

Source: raw/business-model.md · decisions/2026-05-08-blogger-ops-model.md

Upside profile

Asymmetric upside.

SaaS floor. Marketplace compound. Portfolio ceiling.

| Model | Floor | Ceiling |

|---|---|---|

| Pure SaaS | Strong | Capped |

| Pure marketplace | Weak | High |

| Pure portfolio | Weak | Very high · variance |

| @appss | SaaS recurring | Uncapped via portfolio |

If a portfolio app does what Notspy did and goes 10x, we ride 10x — no commission ceiling. If two of them do it, we ride both. Meanwhile, Apps Pro recurring revenue protects the downside regardless.

Source: raw/business-model.md «asymmetric upside» section

Traction · Apps Pro

Cold IG → ~370 sign-ups → ~13 paying customers in 10 days.

Off two viral Reels. Pre-funnel optimisation. Pre-marketplace productisation.

| Metric | Value |

|---|---|

| Visits (recent ~30d) | ~1 500 |

| Sign-ups | ~370 |

| Pro purchases | ~13 |

| Daily Pro purchases | ~3 / day baseline |

| ASP per purchase | $6-17 |

| Hero use-case | Market Research AI |

| Pricing model | Credit-based, shipped 2026-05-08 |

Numbers reflect the funnel before the credit-based pricing shipped. The next viral push hits a different funnel and is expected to convert better. Validation here is trajectory + the new pricing match.

Traction · Notspy proof point

~115K users · ~$7-8K/mo MRR · Telegram just removed our biggest constraint.

Telegram premium-only limit lifted on 2026-05-08. Whole user base can now configure → expecting 2-3× revenue.

- Stack proof: SDK · platform-service · partner programs · referral · influencer onboarding — all on Apps Pro infra

- Funnel evidence: 175 reg → 9 premium → 3 configured today. With premium-limit removed, the 9 → ~all-of-175 path opens.

- Operator transparency: we caught a payment bug 2026-05-08 same week, ship-fixed it. Russia-block hit pre-9-May; recovering.

The 2026-05-08 Telegram update lifting Notspy's premium-only constraint is a structural unlock, not a marketing event. The bottleneck (only Premium users could configure → only ~5% of registered) just disappeared.

Validation arc: if Apps Pro can power Notspy through this transition, it can power any portfolio company's app through similar structural shifts.

Traction · Inbound flywheel

~50 micro-influencers onboarded.

30 / 20 / 50 commission. Productises into stream #4.

- ~50 micro-influencers onboarded (~20+ in past week alone)

- 30 / 20 / 50 — blogger / manager / platform

- Two viral Reels drove most of the recent surge

- 600-700K total Reels views

- 24% interest rate — 50 of 230 viewers ready for training

- Productisation in flight: in-Apps-Pro influencer marketplace

The 50 onboarded names are relationship capital — defensible. Standardised terms create switching cost. The marketplace, once shipped, becomes the network-effect lock.

Why now

Durov is back to TON.

- TON Foundation closed. TON ≡ Telegram. Durov central again.

- Telegram = largest TON validator (~$400M staked, recent weeks).

- Marketing budgets in the ecosystem unlock.

- Founders scrambling to ship — they need a stack — that's Apps Pro.

Investor read: «institutional belief in TON came back; marketing budgets unfreeze; we're early on the curve».

Why now

Telegram Functions + agentic-dev wave.

- Telegram Functions (beta) — hosted bot logic, mini-IDE.

- Bot-managed-bot — designed for AI agents.

- Cursor / Claude Code / Replit bring vibe-coders into Telegram.

- Gap: none speak

init_data, Stars, channel distribution. - Apps Pro fills it. Market Research = entry use-case for vibe-coders who hit the wall.

Narratives align without competing — Telegram amplifies the platform, Apps Pro captures the gap.

Why now

Telegram is resilient — incumbents in TG-strong regions don't get displaced.

Russia · China · Iran. Three different displacement attempts. Telegram retained dominance in all three. Closes the «what if a region blocks Telegram» objection in one slide.

The right framing is resilience as a moat: in regions where Telegram has dominance, alternative messengers and government-backed displacements have repeatedly failed to capture share. This is not just «Russia is fine» — it's the structural durability of the audience layer we sit on.

If Russia escalates to full infrastructure block, exposure increases. Other regions (CIS-non-RU, India, SEA, Africa, global English) absorb risk.

Team

Mark · Anton · CTO + small team.

- Mark — Founder / CEO. Tone-era track record. Notspy ship (115K). Apps Pro live. Picks up founder-pain directly until it ships as product.

- Anton — Head of Bloggers / Marketing. All influencer / blogger ops; 30/20/50 commission.

- CTO — Engineering across Apps Pro · platform-service · builder-api · SDK.

- Engineering core: Vanya · Bogdan · Slava — small, deliberately.

- Content team: Mark + Misha + Anton + ~50 micro-influencers.

Hiring philosophy: cut fast when revenue/spend is tight; avoid «monkey-job» roles that don't surface founder-level pain; promote direct-mandate ownership.

Ask

Early seed. Not bridge. Not pre-seed.

| Item | Value |

|---|---|

| Stage | Early seed |

| Round size | [TBD — Mark] |

| Valuation | [TBD] |

| Lead targets | [TBD] |

Use of funds

- Runway past stabilisation point (~$30-35K/mo)

- Productise inbound flywheel into in-Apps-Pro influencer marketplace

- Grow App Store DAU → unlocks traffic sales

- Ship Apps Pro Bot + Support module + Teams update

- Launch Apps Pro Academy

- AI cost optimisation on Market Research

Looking for investors who get Telegram-native, the asymmetric-upside structure, and want to be early on the macro curve.